From the PM Desk - The Hidden Mechanics of the SpaceX IPO

Key Takeaways

- Big valuation, limited exposure: SpaceX debuted with a valuation approaching $1.8 trillion, but its weight in portfolios will be limited because of an unusually low float

- Indexes are fast-tracking inclusion: Index providers, with the notable exception of the S&P 500, are structurally changing their rules to include SpaceX much quicker than usual

- Billions of dollars of stock are coming to the market: SpaceX will feature a staggered expiration of the lock-up schedule, creating massive selling pressure as shares shift from insiders to the public market

- Patience is an advantage: Newly public companies often fail to live up to expectations, and chasing the stock at IPO is sub-optimal

When SpaceX went public on Friday, June 12, it entered the market as one of the largest companies ever to list, with a valuation of $1.77 trillion. For investors, that headline immediately raises practical questions: how much SpaceX do I actually own? Is it one of the largest positions in my diversified portfolio? Do I own any at all—and if not, is that a problem?

The answer to most of these questions depends less on valuation and more on structure. Specifically, it depends on how much stock is available to trade and how indices incorporate new companies.

Why Size Doesn’t Equal Exposure

At the time of the IPO, only about 4% of SpaceX shares were available to public investors, roughly $75 billion in tradable stock against a multi-trillion-dollar valuation. The rest of the shares are held by insiders—founders, employees, and early-stage investors.

Both numbers matter. Four percent is unusually low. Seventy-five billion dollars is unusually large.

Start with the float, which are the shares actually available for public investors to buy and sell. Most companies in major indices have floats of 90% or higher. IPOs tend to be lower due to lockup periods, which restrict insiders from selling immediately after listing. Even so, SpaceX sits at the extreme. In 2025, about one-third of IPOs had a float under 30%. SpaceX is far below even that range.

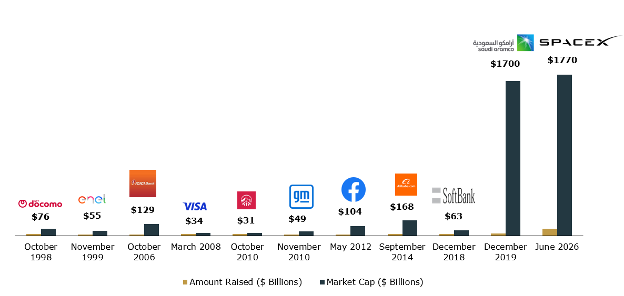

Now consider the dollar amount. At $75 billion, this is the largest IPO ever by proceeds raised. Most large IPOs historically floated closer to 20–30% of shares and raised between $15 billion and $20 billion. The only comparable case is Saudi Aramco, which also combined a massive valuation with a very small float.

Top IPOs of All-Time

Date of Listing and Market Cap ($ Billions)

Past performance is not a reliable indicator of current or future results. Source: Kestra Investment Management with data from Renaissance Capital. Data as of May 20. 2026.

Index providers understand this tradeoff. They do not weigh companies based on total market value. Instead, they use float-adjusted market capitalization, which reflects only the shares investors can actually buy. In simple terms, indices measure what is available on the shelf—not what remains in storage.

That design is intentional. It aligns index weights with real supply and demand. A company with limited tradable shares will have a limited weight, regardless of its size on paper. In SpaceX’s case, that means its presence in most portfolios starts small.

Where Exposure Shows Up First

The timing of that exposure varies across indices, and recent changes suggest the industry is placing a growing emphasis on speed.

Index providers like FTSE Russell, MSCI, and NASDAQ are changing rules to allow inclusion within days if a company meets a minimum threshold based on float-adjusted size. FTSE Russell followed with its own accelerated process, announced in late May, allowing large IPOs to enter the Russell 1000 shortly after listing if there is a credible path to increased float.

The Nasdaq 100 has taken the most aggressive approach. It compressed its inclusion window from what was historically three to twelve months down to just 15 trading days. It also removed its prior 10% minimum float requirement, clearing the way for a company like SpaceX—despite only about 4% of shares trading—to enter quickly.

These changes ensure that index funds will own SpaceX sooner rather than later.

Faster inclusion pulls passive demand forward into a period when markets are still absorbing supply and forming a clearer view on valuation. Earlier index rules, which required longer seasoning periods or higher floats, effectively forced a delay between an IPO and broad index ownership. That gap gave the market time to digest new supply, allowed additional shares to come available, and reduced the risk of concentrating flows into a thinly traded stock.

The newer approach compresses that process. Index providers are not just observers—they are now active participants in how quickly capital moves into newly listed companies. For investors, this makes index methodology stand in stark contrast to “passive”. It becomes a driver of both timing and price sensitivity around major IPOs.

The S&P 500 remains the exception. It has decided to maintain its seasoning period and profitability requirements, slowing SpaceX’s path into the index. As a result, investors in core S&P 500 funds will gain exposure later than those tracking faster-moving benchmarks.

Supply, Lockups, and the Flow of Shares

Index timing is only part of the story. The supply of shares entering the market will play an equally important role in shaping outcomes.

SpaceX has structured a staggered lockup schedule rather than a single release. Insider shares become eligible for sale in phases every few weeks, with some releases tied to earnings milestones. The goal is to avoid a single, disruptive wave of selling.

Even so, the cumulative effect remains significant. Over the coming months, hundreds of billions of dollars of stock could move from insiders into public markets. Spreading that supply over time may smooth volatility, but it does not change the direction of travel: more shares, more availability.

This expansion of float has two implications. First, it introduces a steady source of potential selling as early investors monetize their positions. Second, it increases SpaceX’s weight in indices over time, as more shares become eligible for inclusion.

Passive Demand and its Side Effects

At the same time, passive investing continues to shape demand.

Index inclusion creates automatic buying. When a company enters a benchmark, funds that track it must purchase shares, regardless of price. Faster inclusion accelerates that demand and concentrates it into a shorter window.

But that demand does not appear in isolation. Index funds must rebalance to make room. With more than $14 trillion tied to the S&P 500 and Nasdaq 100, adding a company like SpaceX requires trimming other holdings. Those flows can place incremental pressure on existing mega-cap stocks.

The scale is material. As lockups expire and companies become fully reflected in benchmarks, trillions of dollars of additional market capitalization can enter the indexed universe—even if some shares remain closely held. For context, S&P 500 companies have cumulatively repurchased about $1 trillion of stock on a net basis in the last 15 years. A handful of mega-cap IPOs can absorb a meaningful portion of that demand.

Why Patience Still Matters in IPOs

These mechanics reinforce an enduring principle in investing: IPOs tend to benefit from time.

Historically, newly public companies have often delivered uneven results in their early years. Several forces contribute to this pattern:

- Optimistic pricing: IPO valuations often embed strong growth expectations from the outset.

- Information gaps: Insiders retain better insight into the business and control the timing of share sales.

- Rising supply: Lockup expirations steadily increase the number of shares available.

- Compressed demand: Faster index inclusion concentrates buying into a shorter window.

Data helps frame the dynamic. Research from the University of Florida shows that, on average, 65.6% of shares issued in IPOs trade on the first day. IPOs serve two purposes: they raise capital for the company and provide liquidity for early investors. If you buy at the IPO, you are the exit liquidity of early investors.

The Bigger Picture for Portfolios

For most investors, the conclusion is not complicated. A diversified portfolio will incorporate SpaceX over time through standard index exposure. There is no need to chase the stock or make tactical adjustments to “capture” the IPO.

More important is understanding how index construction shapes outcomes. Differences in how indices treat float, how quickly they add new companies, and how they fund those additions can lead to meaningful variation across portfolios that otherwise appear similar.

SpaceX highlights both sides of that shift. Its initial weight remains small because of limited float. But the push toward faster inclusion signals a broader change in how markets handle large IPOs.

For advisors and investors alike, the evergreen principles of diversification, understanding what you own, and allowing time to do its work remain true. With IPOs, patience is often an advantage, not a cost.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.